College Guides

In an era where education is synonymous with opportunity, many consider pursuing a Master's degree a surefire way to advance their careers. However, is it really the golden ticket to success we've been led to believe?

In an era where education is synonymous with opportunity, many consider pursuing a Master's degree a surefire way to advance their careers. However, is it really the golden ticket to success we've been led to believe? In 2006, Congress slashed $12 billion in student lending funds in a desperate attempt to reduce the fiscal budget deficit. Recent studies have shown that student debt is getting out of control, and lawmakers on Capitol Hill have decided to take steps to help ease the burden for students with college loans.

In 2006, Congress slashed $12 billion in student lending funds in a desperate attempt to reduce the fiscal budget deficit. Recent studies have shown that student debt is getting out of control, and lawmakers on Capitol Hill have decided to take steps to help ease the burden for students with college loans. We scoured the globe, reviewed all the student loan refinance providers we could find, and then chose a select few to provide you with the very best. Here's our top list.

We scoured the globe, reviewed all the student loan refinance providers we could find, and then chose a select few to provide you with the very best. Here's our top list. Student loan forbearance is ending in August, and students are freaking out. Based on our recent survey, 50% of student loan borrowers don’t have enough money for their monthly payments.

Student loan forbearance is ending in August, and students are freaking out. Based on our recent survey, 50% of student loan borrowers don’t have enough money for their monthly payments. The Federal Reserve says the median student debt lies somewhere between $20,000 and $24,999—so the $100k is definitely not the norm. In any case, paying off $100,000 in student loans sounds agonizing.

The Federal Reserve says the median student debt lies somewhere between $20,000 and $24,999—so the $100k is definitely not the norm. In any case, paying off $100,000 in student loans sounds agonizing. It’s crazy to think that a subset of student loan borrowers has never faced a single bill, thanks to the continued pause on repayments since March 2020. But, as they say, all good things must come to an end—and so is the case with this temporary relief.

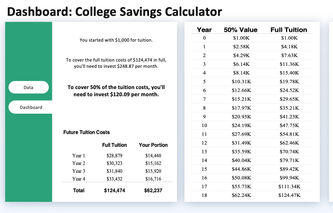

It’s crazy to think that a subset of student loan borrowers has never faced a single bill, thanks to the continued pause on repayments since March 2020. But, as they say, all good things must come to an end—and so is the case with this temporary relief. My wife and I have two kids—ages six and four. We’ve put some money aside for them, but how can we really know how much to save for college?

My wife and I have two kids—ages six and four. We’ve put some money aside for them, but how can we really know how much to save for college? The federal government provides a number of tax breaks that can help ease the financial burden of families saving for college. One of the ways to take advantage of these breaks is by opening a Coverdell Education Savings Account, or Coverdell ESA. At one time these were referred to as Education IRAs, but the Coverdell has a new name and some new rules too.

The federal government provides a number of tax breaks that can help ease the financial burden of families saving for college. One of the ways to take advantage of these breaks is by opening a Coverdell Education Savings Account, or Coverdell ESA. At one time these were referred to as Education IRAs, but the Coverdell has a new name and some new rules too. Each September, high school seniors return to the classroom, while parents begin the process of applying for financial aid. For many of the wealthier families in America, applying for aid will be a waste of time. For those that are financially-challenged, the process can be quite rewarding.

Each September, high school seniors return to the classroom, while parents begin the process of applying for financial aid. For many of the wealthier families in America, applying for aid will be a waste of time. For those that are financially-challenged, the process can be quite rewarding. The Hope Scholarship Credit can help offset the cost of higher education by directly reducing the amount of income taxes paid. The Hope Credit has been around since January 1998, and allows individuals to claim a tax credit of up to $2,500 in qualified education expenses for each student enrolled in school.

The Hope Scholarship Credit can help offset the cost of higher education by directly reducing the amount of income taxes paid. The Hope Credit has been around since January 1998, and allows individuals to claim a tax credit of up to $2,500 in qualified education expenses for each student enrolled in school. Each year, new student loan interest rates are published. Overall, rates have been relatively low; nothing like those that existed back in the early 1980s. That's good news for students because even though they can do very little to control the rising cost of tuition at their colleges, at least the interest rate on their student loans are reasonable.

Each year, new student loan interest rates are published. Overall, rates have been relatively low; nothing like those that existed back in the early 1980s. That's good news for students because even though they can do very little to control the rising cost of tuition at their colleges, at least the interest rate on their student loans are reasonable. The Canadian government has set up the National Student Loan Center (Centre) to ensure its students have access to all the information they need to apply for, and repay, their student loans. The center is conveniently housed in an online website that includes all of the tools, applications, and resources that Canadian students need to manage their loans.

The Canadian government has set up the National Student Loan Center (Centre) to ensure its students have access to all the information they need to apply for, and repay, their student loans. The center is conveniently housed in an online website that includes all of the tools, applications, and resources that Canadian students need to manage their loans. As families make arrangements to send their children off to college, those plans need to include saving money to pay for college expenses too. It's important for families to understand how much financial aid they're going to receive, as well as their expected family contribution.

As families make arrangements to send their children off to college, those plans need to include saving money to pay for college expenses too. It's important for families to understand how much financial aid they're going to receive, as well as their expected family contribution. One of the ways college graduates can ease their financial burden each month is by selecting the appropriate repayment option. This is especially true if the former student is struggling to find a job after graduation. In this article, we're going to be discussing the options available to former students responsible for repaying their loans. As part of that discussion, we'll first talk about repayment timelines and the counseling available before leaving school. Then we'll describe the variety of repayment options available for each loan type.

One of the ways college graduates can ease their financial burden each month is by selecting the appropriate repayment option. This is especially true if the former student is struggling to find a job after graduation. In this article, we're going to be discussing the options available to former students responsible for repaying their loans. As part of that discussion, we'll first talk about repayment timelines and the counseling available before leaving school. Then we'll describe the variety of repayment options available for each loan type. Students looking for help with rising college costs are often told by their school's financial aid department to apply for an ACS Student Loan. In this article, we'll take a closer look at the services this company has to offer students, universities, and financial institutions. Affiliated Computer Services, Inc., or ACS, specializes in business process outsourcing (BPO) and technology outsourcing solutions. According to a press release:

Students looking for help with rising college costs are often told by their school's financial aid department to apply for an ACS Student Loan. In this article, we'll take a closer look at the services this company has to offer students, universities, and financial institutions. Affiliated Computer Services, Inc., or ACS, specializes in business process outsourcing (BPO) and technology outsourcing solutions. According to a press release: There are several circumstances that allow current, and former, students to qualify for loan deferment. These options will vary depending on the types of loans outstanding as well as the borrower's financial and workplace status. A deferment means no payments need to be made on a student loan during the approved deferment period; the payments can be delayed until a later date. In the case of Subsidized Stafford Loans, interest charges will not accrue during this period which means the size of the loan will not grow due to financing charges.

There are several circumstances that allow current, and former, students to qualify for loan deferment. These options will vary depending on the types of loans outstanding as well as the borrower's financial and workplace status. A deferment means no payments need to be made on a student loan during the approved deferment period; the payments can be delayed until a later date. In the case of Subsidized Stafford Loans, interest charges will not accrue during this period which means the size of the loan will not grow due to financing charges. Back in 2005, the Wall Street Journal and the Washington Post reported Congress was going to once again try to close a student loan loophole that's existed since the 1980s.

Back in 2005, the Wall Street Journal and the Washington Post reported Congress was going to once again try to close a student loan loophole that's existed since the 1980s. Sallie Mae was created in 1972 as a government-sponsored enterprise to enhance public access to higher education by serving as a secondary market, and warehousing entity, for student loans. The company offers existing and former student borrowers a wide variety of services, including securing private student loans and debt management.

Sallie Mae was created in 1972 as a government-sponsored enterprise to enhance public access to higher education by serving as a secondary market, and warehousing entity, for student loans. The company offers existing and former student borrowers a wide variety of services, including securing private student loans and debt management. If you've ever felt helpless against the rising cost of college tuition, you're not alone. Fortunately, there is an answer to this problem in the form of 529 plans, which offer individuals saving for college a prepaid tuition option. That's great news for parent-investors looking to lock in the cost of college tuition, since it provides their children with a large choice of private colleges and universities.

If you've ever felt helpless against the rising cost of college tuition, you're not alone. Fortunately, there is an answer to this problem in the form of 529 plans, which offer individuals saving for college a prepaid tuition option. That's great news for parent-investors looking to lock in the cost of college tuition, since it provides their children with a large choice of private colleges and universities. Going to college is a great career move, but it's also an expensive one. Applying for a student loan is a necessity for most families. This article is going to be one of the "all you need to know about applying for a student loan" summaries. It's going to explain how long it takes to apply, and what kind of information is needed when filling out an application.

Going to college is a great career move, but it's also an expensive one. Applying for a student loan is a necessity for most families. This article is going to be one of the "all you need to know about applying for a student loan" summaries. It's going to explain how long it takes to apply, and what kind of information is needed when filling out an application. Service payback and loan forgiveness programs can help former students that are struggling to pay back their loans. These programs are designed to attract individuals to serve in certain jobs, or work in regions of the country, that are experiencing a shortage of talented workers.

Service payback and loan forgiveness programs can help former students that are struggling to pay back their loans. These programs are designed to attract individuals to serve in certain jobs, or work in regions of the country, that are experiencing a shortage of talented workers. Former students can leverage economies of scale by consolidating their federal loans into a single monthly payment. This process helps students save on interest expense, and provides the convenience of managing only one student loan each month.

Former students can leverage economies of scale by consolidating their federal loans into a single monthly payment. This process helps students save on interest expense, and provides the convenience of managing only one student loan each month. As tax time rolls past, parents may be wondering if the interest on a student loan is deductible on their federal income tax return. This article explains how to qualify, deduction rules, phase out limits, as well as providing links to the proper tax forms.

As tax time rolls past, parents may be wondering if the interest on a student loan is deductible on their federal income tax return. This article explains how to qualify, deduction rules, phase out limits, as well as providing links to the proper tax forms.

Student Loans

Moneyzine Editor

December 6th, 2023

Here’s a whopping list of 250+ sales statistics across 25 different categories. We’ve scoured numerous rabbit holes on the internet, scanned reports, and examined credible studies, to compile the most comprehensive list of sales statistics. We raked through the most trusted sources, like The Harvard Business Review, The Pew Research Center, HubSpot, and more, so you don’t have to.

Deepti Nickam

December 1st, 2023

We all want to make more money. But that doesn’t mean college is for everyone. Between rising student loan costs and the need for more trade skills, you don’t have to study for 4+ years to get a well-paying job. In this article, we’re highlighting 20+ jobs that pay 50k a year without a degree.

Kimberly Studdard

November 30th, 2023

Looking for jobs that pay 70k a year without a degree? It's a good search to make because it's definitely not a pipe dream. Some people go to college, pay tens of thousands of dollars, and get a job that maxes out at $40,000 a year. It just makes absolutely no sense! Why not instead get into a career field that can earn $70k a year or more?

Derek Sall

April 18th, 2024

If you’re after a career in the power industry, your job hunt won’t be a waste of energy. You can get ex-static about the opportunities because you’ll be shocked by what’s out there for people with your potential.

Lauren Bedford

April 18th, 2024

Most of us wouldn’t mind making a few extra bucks (or a lot more) every month. It used to be you had to work your full-time job, and that was it. But now, new types of side hustles pop up all the time!

Derek Sall

March 20th, 2024

Your fresh job offer letter says you’ll make $60,000 a year—and you can’t help but wonder how much you’ll earn an hour, a day, and a week. What will your lifestyle look like? And how much of this will go toward the dreaded taxes?

Deepti Nickam

April 18th, 2024

Are lawyers rich? People will automatically bring up lawyers when describing “successful, wealthy people.” But if you look at Forbes wealthiest people list, there are relatively few, if any, lawyers among them. Instead, investors, business leaders, property owners, and oligarchs fill the ranks. Why is this?

Kimberly Studdard

April 18th, 2024

It’s been a rocky time for the average employee. After a global pandemic, more people than ever have quit their job or abandoned the office to work from home. The big question is, has all the uncertainty affected how much work people do?

Derek Sall

March 20th, 2024

Work-life balance has always been a hot topic for discussion, but it was pushed further into the spotlight after Covid-19 forced many workers and students into lockdown. As boundaries between work and home life became blurred, many struggled to maintain a healthy balance.

Lauren Bedford

April 2nd, 2024

The workforce is important—so much so that the United States citizens seem to drop everything when the weekly jobless claims are reported each Thursday.

Derek Sall

November 30th, 2023

Is DoorDash a good side hustle? Yes, it is. How much can you make with DoorDash? Reports say $15–$25 an hour. But that’s before taxes, gas, and other fees. We’ll give you all the numbers to help you decide.

Derek Sall

March 20th, 2024

What if we told you there’s a magical band-aid that can prevent you from bleeding out of cash during a recession, job loss, and most other worst-case scenarios? That band-aid is a financial cushion—liquid investments and saved-up cash for a rainy day.

Deepti Nickam

March 20th, 2024

It should come as no surprise that happier workers perform better. However, if you need numbers and studies to show your boss — we compiled a list of job satisfaction statistics from the most reputable sources out there. If you need more ammo, you’ll also find numbers on job dissatisfaction, worker happiness and productivity, satisfaction rates by industry, and satisfaction rates by country. Read on — you’ve got this!

Dunja Radonic

December 5th, 2023

Since the start of the pandemic in 2020, the popularity of remote work has been off the charts. Companies had no choice but to take advantage of working remotely because employees could not physically come into the office. However, as our selection of remote work statistics will show, remote work continues to be a large part of the new work environment even when the pandemic isn’t in full swing.

Martynas Pupkevicius

April 20th, 2026

Let's face it; earning enough money to pay your monthly bills and fund a retirement account is the start of the financial planning process. We've recognized the importance of developing a career to maximize you earning potential. Our career development section contains information that should help you find a good job and be successful.

Moneyzine Editor

December 6th, 2023