Definition

The financial accounting term journalization is used to describe the process of recording transactions and events. Journal entries are usually chronological lists of debits and credits to accounts, along with a description of the transaction.

Explanation

Transactions are usually not entered directly into the company's general ledger because they involve both a debit and credit to accounts, which are found in two different sections, or pages, of the ledger. The journal allows a company to retain both the debit and credit involved with a transaction in one place.

An entry in a journal is comprised of four parts:

Date of the transaction or event

Account to be debited

Account to be credited

Brief explanation of the transaction or event

Journal entries are subsequently posted to the general ledger as part of the accounting cycle.

Example

On January 15th, 20XX, Company A purchases $500,000 in meters from its supplier Company XYZ, payable in 90 days. The following entry would be made in Company A's journal.

Date | Account Description | Account Number | Debit | Credit |

1/15/20XX | Meters | 380 | 500,000 | |

Accounts Payable | 232 | 500,000 | ||

Purchase of $500,000 in meters from Company XYZ, payable in 90 days. | ||||

Related Terms

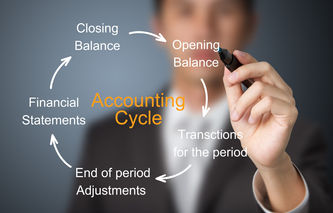

The term accounting cycle refers to the framework and processes followed in each accounting period. The accounting cycle begins with the identification of events and transactions, and ends with the after-close trial balance.

The term accounting cycle refers to the framework and processes followed in each accounting period. The accounting cycle begins with the identification of events and transactions, and ends with the after-close trial balance. Moneyzine EditorNovember 6th, 2024

Moneyzine EditorNovember 6th, 2024 The accounting industry generates billions of dollars. Accounting industry statistics indicate the size of the accounting industry was $544.06 billion in 2020. It gives us an idea of how many accounting events and transactions occur every day in the world. In this article, we will explain what are accounting events and transactions. The term accounting event refers to a change in an item that should be reflected in the company's financial statements. Accounting events can be internal or external and usually involve a change in assets, liabilities, revenues, expenses or owner's equity.Moneyzine EditorDecember 12th, 2023

The accounting industry generates billions of dollars. Accounting industry statistics indicate the size of the accounting industry was $544.06 billion in 2020. It gives us an idea of how many accounting events and transactions occur every day in the world. In this article, we will explain what are accounting events and transactions. The term accounting event refers to a change in an item that should be reflected in the company's financial statements. Accounting events can be internal or external and usually involve a change in assets, liabilities, revenues, expenses or owner's equity.Moneyzine EditorDecember 12th, 2023 The accounting industry generates billions of dollars. Accounting industry statistics indicate the size of the accounting industry was $544.06 billion in 2020. It gives us an idea of how many accounting events and transactions occur every day in the world.Moneyzine EditorNovember 6th, 2024

The accounting industry generates billions of dollars. Accounting industry statistics indicate the size of the accounting industry was $544.06 billion in 2020. It gives us an idea of how many accounting events and transactions occur every day in the world.Moneyzine EditorNovember 6th, 2024- The financial accounting terms real and nominal refer to permanent accounts that appear on the balance sheet (real) as well as temporary accounts that appear on the income statement (nominal).Moneyzine EditorSeptember 21st, 2023

- The financial accounting term posting to the ledger refers to the process of analyzing the credits and debits appearing in journal entries, and recording those transaction amounts in the proper accounts found in the company's general ledger.Moneyzine EditorSeptember 20th, 2023

The financial accounting term general ledger refers to a physical or electronic document that contains a record of the company's financial accounts. Companies can have subsidiary ledgers in addition to their general ledger.Moneyzine EditorNovember 6th, 2024

The financial accounting term general ledger refers to a physical or electronic document that contains a record of the company's financial accounts. Companies can have subsidiary ledgers in addition to their general ledger.Moneyzine EditorNovember 6th, 2024- The financial accounting term special journals refers to a series of dedicated documents used by smaller businesses to chronologically record transactions before posting to the general ledger. Typically, these special journals include the following categories: cash receipts, credit sales, purchases on account, and cash payments.Moneyzine EditorSeptember 21st, 2023