Definition

The accounting industry generates billions of dollars. Accounting industry statistics indicate the size of the accounting industry was $544.06 billion in 2020. It gives us an idea of how many accounting events and transactions occur every day in the world.

The term double-entry accounting refers to the rules by which transactions and events are recorded. Double-entry accounting specifies that for every entry appearing on the left side (debit) of an account, there needs to be a corresponding entry on the right hand side (credit) of an account.

Explanation

There are five high-level accounts that appear on either the balance sheet or income statement: assets, liabilities, owner's equity, revenues and expenses. Debits appear on the left hand side of these accounts, while credits appear on the right. Each time a transaction or event is recorded on the left hand side (debit), there needs to be a corresponding transaction or event recorded on the right hand side (credit) of an account.

Assets and expenses are increased using debits and decreased using credits; while liabilities, owner's equity, and revenues are decreased using debits and increased using credits. The double-entry relationship appears in the tables below:

Asset / Expense | Liability / Owner's Equity / Revenue | |||

Debit | Credit | Debit | Credit | |

Increase (+) | Decrease (-) | Decrease (-) | Increase (+) | |

Example

Company A uses cash (an asset) to pay off a short term liability of $5,000. The double-entry records of this event would be a credit to cash of -$5,000 and a debit to short term liabilities of $5,000 as shown below:

Asset (Cash) | Liability (Short-Term Liabilities) | |||

Credit | Debit | |||

-5,000 | 5,000 | |||

An illustration of the double entry system appears below:

Related Terms

The accounting industry generates billions of dollars. Accounting industry statistics indicate the size of the accounting industry was $544.06 billion in 2020. It gives us an idea of how many accounting events and transactions occur every day in the world. In this article, we will explain what are accounting events and transactions. The term accounting event refers to a change in an item that should be reflected in the company's financial statements. Accounting events can be internal or external and usually involve a change in assets, liabilities, revenues, expenses or owner's equity.

The accounting industry generates billions of dollars. Accounting industry statistics indicate the size of the accounting industry was $544.06 billion in 2020. It gives us an idea of how many accounting events and transactions occur every day in the world. In this article, we will explain what are accounting events and transactions. The term accounting event refers to a change in an item that should be reflected in the company's financial statements. Accounting events can be internal or external and usually involve a change in assets, liabilities, revenues, expenses or owner's equity. Moneyzine EditorDecember 12th, 2023

Moneyzine EditorDecember 12th, 2023 The income statement is a financial accounting report that demonstrates how net income, or profit, is derived from revenues. The main categories appearing on an income statement include revenues, cost of goods sold, operating expenses, non-recurring items and net income.Moneyzine EditorNovember 6th, 2024

The income statement is a financial accounting report that demonstrates how net income, or profit, is derived from revenues. The main categories appearing on an income statement include revenues, cost of goods sold, operating expenses, non-recurring items and net income.Moneyzine EditorNovember 6th, 2024 Also known as a statement of financial position, the balance sheet is used to show the financial health of a company at a particular point in time. The balance sheet consists of assets, liabilities, and owner's equity in the company. It is one of the four key financial statements issued by public companies.Moneyzine EditorNovember 6th, 2024

Also known as a statement of financial position, the balance sheet is used to show the financial health of a company at a particular point in time. The balance sheet consists of assets, liabilities, and owner's equity in the company. It is one of the four key financial statements issued by public companies.Moneyzine EditorNovember 6th, 2024- The financial accounting terms real and nominal refer to permanent accounts that appear on the balance sheet (real) as well as temporary accounts that appear on the income statement (nominal).Moneyzine EditorSeptember 21st, 2023

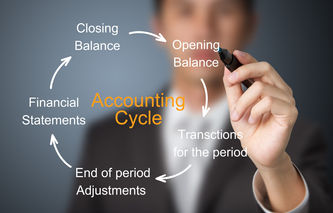

The term accounting cycle refers to the framework and processes followed in each accounting period. The accounting cycle begins with the identification of events and transactions, and ends with the after-close trial balance.Moneyzine EditorNovember 6th, 2024

The term accounting cycle refers to the framework and processes followed in each accounting period. The accounting cycle begins with the identification of events and transactions, and ends with the after-close trial balance.Moneyzine EditorNovember 6th, 2024 The financial accounting term journalization is used to describe the process of recording transactions and events. Journal entries are usually chronological lists of debits and credits to accounts, along with a description of the transaction.Moneyzine EditorJanuary 23rd, 2024

The financial accounting term journalization is used to describe the process of recording transactions and events. Journal entries are usually chronological lists of debits and credits to accounts, along with a description of the transaction.Moneyzine EditorJanuary 23rd, 2024