Definition

The financial accounting term bank credits refers to deposits made to an account such as interest income on a certificate of deposit, or the collection of notes payable. Bank credits are typically identified as part of the monthly bank account reconciliation process.

Explanation

At the end of each accounting period, companies go through a bank statement reconciliation process to understand any differences between the company's record of the account balance and that appearing on the statement issued by the bank.

The reconciliation process involves comparing the company's account balance per the statement received from the bank versus the company's record of cash in the account. Oftentimes the company will not be aware of bank deposits until a statement is received each month. The most common deposits of this type include those associated with interest bearing checking or savings accounts. There can also be electronic deposits of funds from trade partners or investments held by the company.

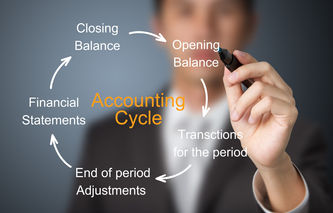

This reconciliation process is part of the accounting cycle, allowing the company to accurately report cash, a current asset, on its balance sheet.

Example

Company A's starting balance in its checking account was $154,300. Company A recorded $123,600 in cash deposits made to its general checking account in the month of September, and withdrawals of $110,500. When the September bank statement was received, it indicated $70 in bank deposits associated with interest earned on its high value checking account. Company A's ending bank balance is calculated as follows:

Bank Account Balance (Starting Balance) | $154,300 |

Add: Deposits | $123,600 |

Less: Withdrawals | $110,500 |

Add: Interest Income | $70 |

Bank Account Balance (Ending Balance) | $167,470 |

Related Terms

The term accounting cycle refers to the framework and processes followed in each accounting period. The accounting cycle begins with the identification of events and transactions, and ends with the after-close trial balance.

The term accounting cycle refers to the framework and processes followed in each accounting period. The accounting cycle begins with the identification of events and transactions, and ends with the after-close trial balance. Moneyzine EditorNovember 6th, 2024

Moneyzine EditorNovember 6th, 2024 The financial accounting term current assets is generally defined as cash and other assets that can be converted into cash within one year or one operating cycle, whichever is longer. Current assets are a subcategory of assets, which appear on a company's balance sheet.Moneyzine EditorNovember 6th, 2024

The financial accounting term current assets is generally defined as cash and other assets that can be converted into cash within one year or one operating cycle, whichever is longer. Current assets are a subcategory of assets, which appear on a company's balance sheet.Moneyzine EditorNovember 6th, 2024 All those hours spent playing old PC games when your boss wasn’t looking means you know a thing or two about Solitaire. So why not play for money? If only it were that easy.

All those hours spent playing old PC games when your boss wasn’t looking means you know a thing or two about Solitaire. So why not play for money? If only it were that easy. Lauren BedfordApril 18th, 2024

Lauren BedfordApril 18th, 2024- The financial accounting term reconciliation of bank account balances refers to the process of understanding the difference between the company's records of cash in their account, and the amount appearing on a statement received from the bank.Moneyzine EditorNovember 6th, 2024

The term bank charges and fees refers to the costs applied to an account balance for services such as bank checks, non-sufficient-funds (NSF) check processing, safe deposit box rentals, and overdraft protection. Bank charges and fees are typically identified as part of the bank account reconciliation process.Moneyzine EditorNovember 6th, 2024

The term bank charges and fees refers to the costs applied to an account balance for services such as bank checks, non-sufficient-funds (NSF) check processing, safe deposit box rentals, and overdraft protection. Bank charges and fees are typically identified as part of the bank account reconciliation process.Moneyzine EditorNovember 6th, 2024 The term cash over and short refers to an expense account that is used to report overages and shortages to an imprest account such as petty cash. The cash over and short account is used to record the difference between the expected cash balance and the actual cash balance in the imprest account.Moneyzine EditorJanuary 10th, 2024

The term cash over and short refers to an expense account that is used to report overages and shortages to an imprest account such as petty cash. The cash over and short account is used to record the difference between the expected cash balance and the actual cash balance in the imprest account.Moneyzine EditorJanuary 10th, 2024 The term deposits in transit refers to cash that has been recorded as received by a company, sent to their bank account, but not yet posted to the account's statement by the bank. Deposits in transit are typically identified as part of the bank account reconciliation process.Moneyzine EditorJanuary 15th, 2024

The term deposits in transit refers to cash that has been recorded as received by a company, sent to their bank account, but not yet posted to the account's statement by the bank. Deposits in transit are typically identified as part of the bank account reconciliation process.Moneyzine EditorJanuary 15th, 2024- The term outstanding checks refers to those checks that have been recorded by a company as being written, but not yet cleared and posted to the account's statement by the company's bank. Outstanding checks are typically identified as part of the bank account reconciliation process.Moneyzine EditorSeptember 20th, 2023