The tides are shifting... Up until now, you were focused on paying down debt, career, and maybe even investing. You kept your housing to 25% of your income, your auto loans to no more than 8%. You’ve mastered cash flow management and probably don’t even have to look at your budget anymore. But now you're closing in on that magic number and you're wondering, "Where should I be financially at 40?"

Similar articles:

Where Should You Be Financially at 40 Years Old?

You have wisdom from the mistakes you’ve made. You know what works and what doesn’t work. You’re seeing success in your career and personal finances. You’re working towards stability. Or...maybe you’re not quite there. But, those are all the goals and dreams you hold in your head that you’re working toward. Age 40 is about the middle between entering the workforce and retiring from it.

So where should you be financially at age 40?Here are 11 financial milestones you want to be looking at once you hit 40.

1) Have a Solid Emergency Fund

According to a Federal Reserve Survey, 40% of Americans cannot handle a $400 emergency. By 40 years of age, you want to have at least $1,000 in the bank for emergencies. In fact, keeping with the 40% theme, only 40% of Americans could come up with $1,000 in an emergency if they needed to.

So the question you need to ask yourself is, which group are you in? If you're 40 and you don’t have access to $1,000 right now, that’s okay. Knowing more means you can do better. At 40, you probably have a garage or basement with things you definitely don’t use or will never use again (hello, cross country skis). Have yourself a little Craigslist or Marketplace sale, and see if you can turn your stored items into a $1,000 emergency fund.

Unsure where to get started? Check out our 50/30/20 budgeting template, it's perfect for beginners 👇

50/30/20 budget template perfect for beginners!

A few key features of this template:

Only includes the things you need – no unnecessary tabs

Included clear instructions

Pre-filled with sample data

Fully customizable to your needs

2) Three to Six Months of Expenses in Cash

Now that you have your $1,000 emergency fund checked off, by 40 years old you’ll also want 3-6 months of expenses in liquid funds. That means in the bank, ready to go if you have an emergency, or if life happens. Calculate everything it costs you to live in one month. If you haven’t already, create a budget and list the things that you have to spend every month.

Mortgage or rent,

utilities,

internet,

phones,

food,

gas,

clothes,

entertainment,

and any other payments you need to make.

For the average American, this falls somewhere around $4,000. So your fully funded emergency fund should be $12,000-$24,000, plus $1,000 for emergencies. By saving 3-6 months' worth of expenses in case, you’ve created a financial safety net for yourself and your family.

You do not need to go into credit card debt if something happens, and you have a six-month cushion to navigate any major life changes. This is financial strength, and at 40, you deserve that peace of mind.

3) No Debt Except Your Home

Where should you be financially at 40 when it comes to debt? By 40 years old, you ideally want to have no debt, with the exception of a low-interest mortgage.

No credit card debt,

student loans,

car loans,

or loans to friends and family.

Your 40’s represents a turning point here. When you’re under 45, your dollars should be more focused on getting investments set up to take advantage of compound interest, without much thought for aggressively paying down your mortgage.

Once you’re over 45, you want to get rid of that debt once and for all, and that’s when you want to shift to paying down the mortgage as much as you can. You want to be completely financially independent and you don’t want any debt burdens as you head into retirement.

If, at this point, you are still carrying other major debts, it’s time to get super serious about eliminating them. Debt is keeping you from being able to save, give, and do whatever it is you want to do. Start your debt snowball, or avalanche, or your preferred method.

Most people can get out of debt in a focused 18-24 months. Get intense about it, make a chart, or whatever keeps you motivated, don’t focus on saving and investing, focus only on getting out of debt.

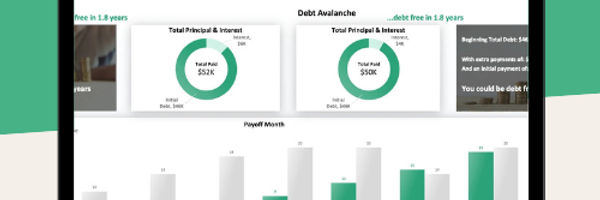

We've created many debt payoff spreadsheets to help you tackle your debt, but this is our favourite 👇 It includes both, avalanche method and debt snowball, so you can easily try both and see what works for you.

The debt snowball or the debt avalanche? This template will give you answers 💡

This template is:

Compare which method works for YOU

Fully automated and beginner-friendly

Includes both, debt snowball and debt avalanche templates in one with all the features!

Read more:

4) Three Times Your Salary Saved for Retirement

Have you been ignoring your future financial security? Take a second to breathe and relax. This is only a target, and everyone’s financial situation is different. But with peak earning happening in your 40s, now is a good time to take stock of where you stand with this goal. But still, breathe. You still have 20+ years for compound interest to work its magic.

Your 40s is absolutely the time to start maxing out your retirement contribution.

If you have kids, they’re likely now out of full-time day-care, saving you thousands of dollars. At this time, many people are debt free aside from their mortgage, and many people hit their peak earning potential, making it the perfect time for you to throw more money at your retirement account. When you reach your 40s, aim to save at least 10-15% of your income into your retirement (more if you’re playing catch-up), and increase it by 1% per year.

Roth IRA or 401k? This template will answer your questions.

With this template, you will get:

All DFY, simply add your details

Charts for comparison and clear answer

Easily update for any year (2023, 2024, 2025, etc…)

Read more:

5) Start Saving for Your Child(ren)'s College

Wondering where you should be at 40 years old when it comes to saving for your kid's college? If you're just starting, that's okay. Your 40s is a great time to open a 529 savings plan for any children you have. You’re at your max earning potential and have fewer financial responsibilities. Any amount you can contribute can help your children’s college goals in the future.

However, if you have to choose between saving for retirement and saving for your kids' college fund, you have to prioritize your retirement. You don’t want to pay for their education only to be a financial burden to them later in life. After all, there are student loans, but there are no retirement loans. If you can do both, now is a great time to work on that.

Related:

6) Get on The Same Financial Page as Your Parents

For a lot of families, this is not an easy topic to broach. Many parents of a certain age don’t believe in talking about money or don’t want to face that point in their life, or they believe they’re the parent and they don’t need to talk about it with their children. But the truth is, you all need to be on the same financial page as they’re getting older.

Taking care of your parents starts to become a concern for many 40-year-olds...

Are there any expectations for the care your parents need you for?

Are they financially secure, and do they have a plan?

These questions are important because they help you plan for expenses going forward. Now is the time to rip off the band-aid, and find out where everyone stands.

7) Have Disability Insurance

Many people don’t consider this, but according to the Social Security Administration, 25% of people will become disabled at some point in their life. In the event that you become part of that 25%, you want to make sure you and your family are financially taken care of.

Many people can get disability insurance through their employer, and that’s great. But, with the limitations of those policies, it’s best to get supplemental disability insurance.

8) Have a Good Life Insurance Policy

Hopefully, you have a life insurance policy by now, but in the event that you don’t, now is the time (we recommend our affiliate partner, Bestow!). It’s especially important if you have a spouse or children that rely on your income. Keep in mind that in the event of your death, not all debts are forgiven. Something like a mortgage or private student loans will not be forgiven if you die, and you want to make sure the people who are left behind are not saddled with that bill.

Make sure you carry enough life insurance to carry these costs, as well as the cost of your funeral. The older you get, the more expensive your life insurance premiums become, so you’ll want to get it now while the premiums are still at a good price.

9) Complete Estate Planning and Keep Your Will Updated

When you're thinking about where you should be financially in your forties, it’s especially important to think about estate planning, even if you’re not “wealthy”. Have a will in place at the very least, and make sure it gets updated. If you have property and assets, estate planning is crucial to make sure things are properly stated in the event of your death.

Make sure you update your will if there’s a marriage, children are born, if there are any major financial changes or if you move out of the state. Because wills are on a state-by-state basis, you want to make sure everything is in line no matter where you live. Having a will and estate plan in place is the final act of love you can do for your family and friends to make sure everything is taken care of.

10) Have a House Repair Fund

At 40, there’s a good chance you're going to be in your current house for awhile. Because things are not made to last forever, it’s a sure bet that at some point in time you’ll need to repair and replace things in your house.

In your forties, you have the most disposable income in your life, so you might also be thinking about renovations and upgrades. This is the time to have an amount set aside for emergencies or planned upgrades to your home, without having to dip into debt to complete it.

11) Maintain a Great Credit Score

In your 40’s, you hopefully have a pretty solid credit score going. If you don’t, this is a good time to watch it carefully, and see what you can do to build that great credit score, which can take years.

The average person has a credit score of about 711, though anything in the upper 600’s is generally considered good. Of course, there’s no definition of great credit, but a score of 760 or higher will usually get you a lender’s best rate, so that’s a good number to aim for. If you’re already there, keep it up! If you’re not, now is a good time to really put in the effort to maximize your score, and keep it there.

Where to Be Financially at 40 - How Are You Doing?

How are you looking financially in your 40s?

Maybe you’re ticking all these boxes, or nowhere near any of them, or somewhere in the middle, but these are great guide posts to navigate your financial health in your 40s. You might pick one or two that are the most important to work toward and focus intensely, or take baby steps toward all of them.

No matter where you stand, your 40s is the time to take a close look at your financial health, and plan accordingly.

Are you on track with your finances at forty years old? Tell us how you're doing in the comments below!

.jpg)

.jpg)