In a down economy, this story is all too familiar. Individuals wake up one day to find themselves overwhelmed by debt. Money has been spent faster than it's coming into the household. At the extreme, the debt load is so out-of-balance that bankruptcy appears to be the only alternative.

Every day, people face a similar financial crisis. It might be caused by the sudden loss of a job, the onset of an illness, or a pattern of overspending. But this financial situation doesn't have to go from bad to worse.

If you're ready to tackle your debt, I recommend starting with one of our templates 👇

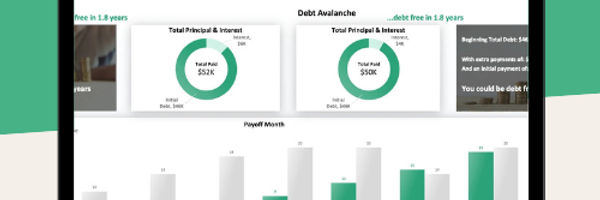

The debt snowball or the debt avalanche? This template will give you answers 💡

This template is:

Compare which method works for YOU

Fully automated and beginner-friendly

Includes both, debt snowball and debt avalanche templates in one with all the features!

Eliminating Debt

Additional Resources |

Getting out of Debt Invest or Pay Down Debt Prepaid Debit Cards Credit versus Debit Cards |

There is a short list of viable options to eliminate or control the source of debt problems. This includes developing a budget, credit counseling, negotiating with creditors, consolidation loans, and even bankruptcy.

This article will quickly review each choice, starting with the self-help options of budgeting and negotiation. Next, we'll look at the options that make use of external resources such as credit counseling, consolidation, and bankruptcy.

Budgets

A high-level budgeting process starts with a list of the household's income sources. The next step is to identify expenses. The key to a viable budget is to separate mandatory expenses from discretionary (optional) ones. Examples of mandatory expenses include rent, mortgage payments, travel expenses to work, utilities, auto loans, and insurance premiums.

Discretionary expenses are those a household could eliminate, or reduce, if necessary. Expensive clothing, gifts, jewelry, restaurants, lavish vacations, and entertainment are good examples of discretionary expenses. The last step in the process is subtracting expenses from income and making sure the "money in" is greater than "money out."

Sources of income should be easy to identify, as will the home's mandatory expenses. The best place to start with discretionary costs are past credit card statements. Assembling the data just takes time, perseverance, and a worksheet to track progress. This website has three articles dedicated to this topic, including detailed instructions as well as spreadsheets that can be downloaded too:

Family Budget Basics: explains how to create a budget, and compare it to national average spending patterns.

Budget Worksheet: a two-part series, describing how to put together a budget, as well as a spreadsheet that can be downloaded.

Household Budget: a final "how to" article that emphasizes mandatory versus discretionary expenses as well as providing a personal budget example.

Monthly Budget Template: a customizable spreadsheet for monthly budgeting, suitable for personal use, couples, and households. For those who'd like to be more flexible in terms of intervals, we also have a simpler budget template.

Home Renovation Budget Template: a downloadable spreadsheet to budget home renovation projects. We also have guides for specific upgrades, including fireplace remodeling, second-story addition over the garage, kitchen remodeling, covered patios, and building sheds.

Credit Card Payoff Spreadsheet: a downloadable spreadsheet to track credit card debt. You can also use our credit card payoff calculator to come up with a payoff plan for your debt.

Debt Avalanche Spreadsheet: a debt tracking spreadsheet to apply the debt avalanche method.

Debt Snowball Spreadsheet: a debt tracking spreadsheet to apply the debt snowball method. If you'd like to learn more about both methods, we compare debt snowball and avalanche tactics here. You can also use our debt snowball vs avalanche calculator to find out which works better for you.

You can find more personal finance tools and products here.

Or you can grab yourself a copy of our top debt template 👇

The debt snowball or the debt avalanche? This template will give you answers 💡

This template is:

Compare which method works for YOU

Fully automated and beginner-friendly

Includes both, debt snowball and debt avalanche templates in one with all the features!

Negotiating Settlements with Creditors

Creditors may agree to negotiate with individuals when they feel this is in their best interests. For example, they might be more likely to negotiate with someone if they believe that person is a good candidate for bankruptcy.

Credit card companies will settle in the range of 10 to 50% of outstanding debt, but this agreement needs to be negotiated. The settlement process can take anywhere from three to nine months.

It's also possible to contact companies to request more realistic payment arrangements. For example, someone might be carrying a balance of $300 on their water bill. Instead of trying to pay the entire amount in one lump sum, they may be able to negotiate a deferred payment arrangement, or DPA. This type of arrangement allows the debtor to pay off the $300 over a longer period of time.

Keep in mind these companies want to collect all money owed. Forgiving this debt, or making an arrangement, will take some work. The best approach is an honest one. Agreeing to an arrangement that is unrealistic will only make the next round of negotiations tougher.

In fact, many individuals are not equipped to deal with creditors and prefer to seek the help of a professional.

Credit Counseling

Individuals struggling to stick to a budget, or those that are not really sure how to create a realistic budget might want to consider contacting a credit counseling organization. Many counselors work for nonprofit organizations that are well-equipped to help families solve their financial problems.

Our article on debt counseling outlines a process for identifying a legitimate credit counselor. But as mentioned in that article, just because an organization says it's a "nonprofit," does not mean its services are free.

Remember, the goal here is to eliminate debt, not make it grow. Good counselors will have a methodical approach to solving a family's financial problems, many of which are the same as those mentioned in this article.

Consolidating Debt

The process of taking individual "loans" and assembling them into one larger loan is known as debt consolidation. While this process does nothing to eliminate debt, it helps debtors to understand how much money they owe creditors. It also allows them to manage one monthly payment, oftentimes with more attractive interest rates than smaller loans.

For example, someone might have balances on several credit cards in addition to student loans or a monthly car payment. A consolidation loan puts all these financial obligations together in one place, leveraging the lower interest rates offered with the consolidated loan. This type of arrangement usually provides an income tax advantage over personal loans too.

Lenders will require collateral, and a home is the likely choice. Unfortunately, if the borrower falls behind on payments, they're putting the loss of their home at risk. It's important to understand the terms and conditions of a loan before entering into any agreement with a lender.

Calculators and Tools

This website has a number of online calculators that can help model the payments owed on a consolidation loan. This includes a debt reduction, consolidation loan, and a credit card payoff calculator.

Bankruptcy

Filing for bankruptcy is not the easiest way to eliminate debt, and it can be a painful choice too. It's possible to lose a home, car, and still wind up owing companies money. Legal fees are expensive, and judges don't always show compassion.

Unlike businesses, individuals can file for Chapter 13 or Chapter 7 bankruptcy. The difference being that Chapter 13 involves a plan to reorganize a household's finances, thereby positioning it to pay down debt. Chapter 13 can also involve a debt management plan, or DMP. The successful completion of this plan can result in debt forgiveness. But this can be a long and financially stressful process.

Anyone seriously considering this solution needs the advice of an attorney since bankruptcy is a legal proceeding.

About the Author - Debt Elimination

.jpg)

.jpg)