Young adults are taught many things in school, but simple home economics concepts like balancing a budget are often overlooked. Without a plan, it's nearly impossible to meet the savings goals individuals and families need to reach their financial freedom. In this article, we're going to explain the basics of household budgeting. This includes how to identify a home's sources of income as well as mandatory and discretionary expenses. We're also going to talk about savings targets, and why they're important. Finally, we're going to finish up with a template that everyone can use to create their own monthly budget.

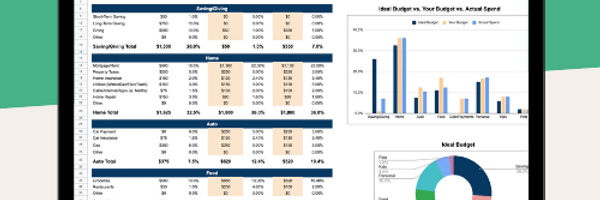

Simple, quick, and easy monthly budget template for Google Sheets and Excel.

With this template, you will get:

Pre-set expense categories

Simplified dashboard and day-by-day monthly tracker

Automated charts for comparison

Day-by-day views for budgets and actual spend

Household Debt

According to statistics gathered by the Federal Reserve Board, household debt service reached a historical high in the fourth quarter of 2007. The same holds true for the Debt to Net Worth measure. Even today, the average household spends anywhere from 15 to nearly 25% of their disposable income making their debt payments. Unfortunately, around 764,000 households also file for bankruptcy annually (year ending March 2020).

Credit Card Bills

The typical American household is not always prepared to meet the financial challenges of creating a balanced budget. In 2004, Alan Greenspan talked about the growing substitution of credit card debt for personal loans. The average consumer no longer has to seek the approval of a bank to gain access to an unsecured loan. They can use their credit card for a variety of new purposes, including borrowing money.

Balancing a Budget

Individuals that fall behind on their monthly payments need to learn the basics of creating a budget. The first rule of thumb for a financially sound home is simply this: Household Income must be greater than Household Expenses Budgeting 101, right? It's surprising how many families break this simple rule. When it's broken, the household needs to borrow money to pay its expenses. That is a short-term strategy that can lead to long-term problems if it happens every month.

Pay Yourself First

Some individuals believe that income only has to equal expenses for a household budget to be balanced. That's true if someone plans to work forever. But plans for the long-term need to include the concept of "pay yourself first" too. This saying has been around for a long time and it means before paying anyone else, put some money aside for the future. That's something everyone should strongly consider as part of their retirement plan, and household budgeting process.

Creating a Household Budget

The process of creating a household budget allows families to learn about their monthly living expenses. Alternatively, it's possible to use a template that someone else has put together. The learning experience won't be as great, but it'll save time. With either option, the budgeting process can be broken down into three subsections, which include the identification of income, mandatory, and discretionary expenses.

Automate it using budgeting apps

Spreadsheets may not be for everyone - they do require an awful lot of manual work, and there are alternatives out there for folks who simply don't have the time. We listed the most popular budgeting apps and other personal finance tools (a blend of spreadsheets, calculators, and automated applications). It includes some of the industry giants like Mint and YNAB (read through our comparison to find out which suits you the best) - all of which integrate with your online banking app for seamless planning.

Monthly Income

The income portion of a household budget accounts for all of the sources of money that flow into the home. This can include paychecks, interest income, tax refunds, stock dividends, bonus payments, and gifts of money. Any reliable source of money flowing into a household each month should be included in the income section of the budget.

Simple, quick, and easy monthly budget template for Google Sheets and Excel.

With this template, you will get:

Pre-set expense categories

Simplified dashboard and day-by-day monthly tracker

Automated charts for comparison

Day-by-day views for budgets and actual spend

Mandatory Expenses

The monthly costs that are "must pay" are considered mandatory expenses. This includes mortgage payments, car loans or lease payments, and property taxes. All the money owed others as well as expenses such as energy bills and other utilities should also be included in this category.

Life insurance premiums, health care costs, childcare, commuting expenses, groceries, and other costs that help individuals earn income and provide them with a healthy lifestyle are also considered mandatory. These should be the absolute last costs a household would give up. It's important to set aside money for the future too; that's mandatory. It's one of the fundamental rules for a sound financial planning strategy.

Discretionary Expenses

The budgeting process gets more difficult when trying to evaluate discretionary expenses. This part of the process requires families to really think about whether or not to spend money on these items. Examples of discretionary expenses include going out to the movies, entertainment, dining out at restaurants, extravagant vacations, expensive clothing, jewelry, and other luxury items. Monthly credit card bills are oftentimes the best source of information to examine when looking for spending patterns. If they aren't handy, it's usually possible to download past statements from a credit issuer's website. Take a close look at several statements; it's sometimes an eye-opening experience.

Household Savings

Once the sources of monthly income have been identified, and expenses assembled, it's time to figure out if the budget is balanced. The formula used in this example is a simplified calculation of household savings: Household Income - Household Expenses = Household Savings If the value for household savings is negative, there is a budget deficit. If that value is zero, the budget is balanced. If household savings is positive, there is a budget surplus, which is the sign of a "healthy" budget.

Forms, Templates, and Spreadsheets

Anyone that's good at putting a spreadsheet together shouldn't have any problem creating their own budget. Individuals that aren't up to speed on Microsoft Excel, or another spreadsheet application, can use one of the forms we've already put together.

Household Budget Worksheet

As promised earlier in this article, we're going to provide a household budget worksheet that can be downloaded for free: Personal Budget. This document was also included in a two part series called Budget Worksheet. That particular series reviews the topic of putting together a personal budget, and even discusses some of the software options available for purchase such as Quicken.

Average Costs

A household budget can be summarized simply as:

Income - Expenses = SavingsMoneyzine Editor

We also have information for anyone that would like to compare their monthly expenses to that of an average American household. Our family budget template allows end users to create a family budget. It also includes a variance report, which indicates how well actual expenses are tracking against the plan. That spreadsheet was built from an average family budget. This site also publishes a family budget calculator that allows users to compare their monthly household expenses to that of an average household. The information in these tools was based on data gathered by the federal government.

Evaluating a Budget

Once a household budget has been created, it's necessary to track expenses and income. After several months, it's possible to have a good feel for how well actual expenses measure up against those forecasted. Budgets should be reviewed each month. The process should be dynamic, and families need to be prepared to make adjustments to stay within their plan. While it's nice to remove the stress of falling behind on bills, keep in mind that everyone needs to enjoy life too. Changing purchasing habits or downsizing a home makes sense if that's what it takes to balance a budget. People are often surprised at how stress-free life can be when both a budget, and one's life, is in balance.

Additional Resources

Creating a budget is arguably the first line of defense against runaway debt. It provides the end user with a clear picture of both sources of income and household expenses.

Creating a budget is arguably the first line of defense against runaway debt. It provides the end user with a clear picture of both sources of income and household expenses. Idil WoodallDecember 16th, 2024

Idil WoodallDecember 16th, 2024- There is one fact about money most people will agree with: There never seems to be enough of it. Paying bills can be stressful, and the lack of financial resources can strain relationships too. Fortunately, creating a budget can help families to plan their expenses and meet their monthly obligations.Moneyzine EditorDecember 16th, 2024

When household income is greater than household expenses, it's possible to save money, either through small changes or strategic moves. On the other hand, when income is less than expenses, the household is going into debt.Moneyzine EditorDecember 12th, 2023

When household income is greater than household expenses, it's possible to save money, either through small changes or strategic moves. On the other hand, when income is less than expenses, the household is going into debt.Moneyzine EditorDecember 12th, 2023 It's uncomfortable to be in debt; no one likes the feeling of being out of control, especially when it comes to their personal finances. Individuals in this situation have two problems to solve: getting out of debt, and staying out too. In this article, we're going to start by talking about some of the signals that indicate a problem could be on the horizon. Next, we'll explain some of the habits that help individuals to eliminate debt. Finally, we'll talk about the steps borrowers can take to stay out of debt.Moneyzine EditorApril 17th, 2024

It's uncomfortable to be in debt; no one likes the feeling of being out of control, especially when it comes to their personal finances. Individuals in this situation have two problems to solve: getting out of debt, and staying out too. In this article, we're going to start by talking about some of the signals that indicate a problem could be on the horizon. Next, we'll explain some of the habits that help individuals to eliminate debt. Finally, we'll talk about the steps borrowers can take to stay out of debt.Moneyzine EditorApril 17th, 2024